What is Working Capital Management? Essential Guide

Let’s break down what working capital management actually means. Forget the dry, textbook definitions. Think of it as the art of juggling your short-term cash, the stock on your shelves, and the bills you need to pay. It’s all about making sure your business has enough cash on hand to handle its daily grind without breaking a sweat.

Getting this right isn’t just a “nice-to-have” financial skill; it’s absolutely crucial for keeping your business healthy and running smoothly.

Why Working Capital Is Your Business’s Lifeblood

Picture your Auckland business as a popular café. The money you make selling flat whites and avo toast is your revenue, sure. But your working capital is the cash that actually keeps the machine running. It’s what you use to pay your baristas, buy fresh coffee beans from your supplier, and cover the rent.

Without it, even a wildly popular and profitable café can find itself in a tight spot, unable to operate.

This is where working capital management comes in. It’s not just boring accounting; it’s the game plan you use to handle your operational cash flow. For any Kiwi business owner, it helps answer some pretty critical questions:

- Can we actually afford to pay our suppliers next month?

- Are we getting paid by our clients fast enough?

- Is our money just sitting on a shelf collecting dust as unsold stock?

A healthy-looking bank balance doesn’t mean much if your cash is all locked up when you need it most. That’s why you have to actively manage it.

The Basic Formula for Success

At its core, working capital management comes down to a simple formula. It’s a quick health check that compares what you own that can easily be converted to cash (current assets) with what you owe in the very near future (current liabilities).

Working Capital = Current Assets – Current Liabilities

If the number is positive, you’re generally in a good spot to cover your immediate bills. But the real goal is to find that perfect sweet spot—not having too much cash sitting idle, but never having too little.

Let’s break that down even further.

The table below shows what we mean by current assets and liabilities in the context of a small Auckland business.

Core Components of Working Capital

| Component Type | What It Is | Auckland Business Example (e.g., a local retailer) |

|---|---|---|

| Current Asset | The money in your bank account, ready to be used. | Cash from weekend sales at your Ponsonby Road shop. |

| Current Asset | Money owed to you by customers for goods/services already delivered. | Invoices sent to a corporate client for a large gift basket order. |

| Current Asset | The value of the products you have on hand to sell. | The stock of Kiwi-designed clothing hanging in your Newmarket store. |

| Current Liability | Money you owe to your suppliers for goods or services. | The bill from your local coffee roaster for this month’s bean supply. |

| Current Liability | Short-term loans or lines of credit that are due soon. | A small business loan payment due at the end of the month. |

| Current Liability | Upcoming bills like rent, utilities, and employee wages. | The monthly rent for your retail space and the fortnightly payroll. |

Understanding these moving parts is the first step to taking control of your cash flow and ensuring you have what you need, right when you need it.

More Than Just a Local Concern

This isn’t just a headache for businesses here in Auckland; it’s a challenge business owners face all over the world. In fact, the global market for working capital management is growing as more companies use technology to get a better handle on their finances.

Everyone is trying to fine-tune their short-term assets and liabilities to improve their cash position. If you’re curious about the tech side of things, you can explore more insights on working capital trends. It all points to one simple truth: mastering your day-to-day cash flow is fundamental to success, whether you run a local shop in Mount Eden or a massive global company.

The Three Pillars of Smart Capital Control

Managing your working capital isn’t one single action. It’s more like a balancing act between three crucial areas of your business. I like to think of them as the three pillars holding up your entire financial structure. If one gets shaky, the whole thing can start to feel unstable.

These three pillars are:

- Accounts Receivable: The money people owe you.

- Accounts Payable: The money you owe your suppliers.

- Inventory Management: The stock you have on hand.

Getting these three to work in harmony is the real secret to a healthy, predictable cash flow. For any small business in Auckland, nailing this balance is often the difference between just getting by and truly thriving. Let’s break each one down.

Pillar 1: Accounts Receivable

This is all about the cash that’s coming in—or at least, it’s supposed to be. When you’ve done the work or sold the product but are still waiting for the payment, that outstanding money is an “account receivable.” For most businesses, this is where cash flow gets frustratingly unpredictable.

Let’s say you run a small construction company in Auckland. You’ve just wrapped up a major renovation on a house in Remuera, but your client has 60 days to pay that final, hefty invoice. For two whole months, that cash is out of reach, even though you’ve got wages to pay and new materials to buy.

The goal here is simple: shrink that waiting time without annoying your clients. That means getting your invoices out the door immediately, making it easy for people to pay you, and having a polite but firm process for chasing up anything that’s overdue.

Pillar 2: Accounts Payable

This pillar is the other side of the coin—it’s the money you owe out to your suppliers. Every bill that lands in your inbox, from your software subscription to your raw materials, is an “account payable.”

Now, it might feel responsible to pay every bill the second it arrives, but smart business owners know there’s a bit more to it. You want to hang onto your cash for as long as you responsibly can to keep your own funds flexible.

This could be as simple as negotiating better payment terms with your suppliers. For instance, if you can change your terms from paying within 15 days to 30 days, you’ve just given your business an extra two weeks of cash flow breathing room. Our guide on cash flow principles and management digs deeper into how these timings can make or break your financial stability.

Pillar 3: Inventory Management

If your business sells physical products, inventory is a massive piece of your working capital puzzle. Your stock is basically cash sitting on a shelf. When it sells quickly, it turns back into cash. But if it sits there for months, it’s just tying up money you could be using to grow the business.

Think about a boutique clothing shop in Newmarket. If they’re still holding onto a rack of summer dresses in May, that’s a lot of cash trapped in unsold goods. On the flip side, running out of a bestseller means you’re leaving money on the table.

Strong inventory management is all about finding that perfect balance. You want enough stock to keep customers happy but not so much that your capital is just gathering dust in the back room.

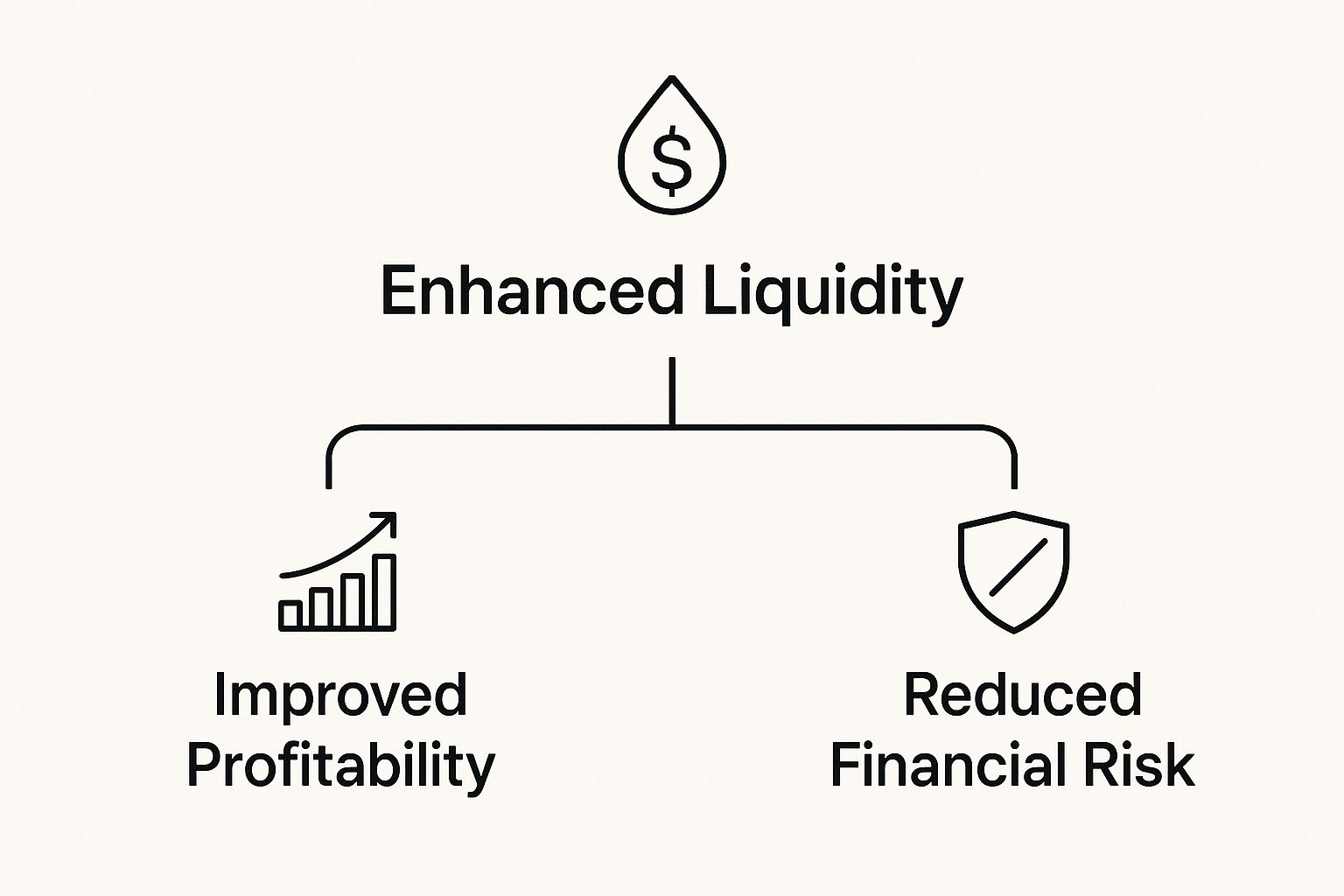

This image really brings home how these three pillars work together to support your business.

As you can see, when you get a handle on these areas, you improve your liquidity. That directly leads to better profitability and a much less risky financial position.

How Good Capital Management Changes the Game

Knowing the nuts and bolts of working capital is one thing. But seeing what it actually does for a business? That’s where things get interesting. This isn’t just about keeping the lights on; it’s a powerful strategy that separates the businesses that just get by from the ones that truly get ahead.

Let’s picture two similar businesses right here in Auckland. One is on top of its working capital. The other… not so much. Their stories will unfold very differently.

The first business keeps its cash flowing smoothly, which means it has the money ready to jump on opportunities. When a supplier offers a massive 20% discount for a bulk buy, they can say yes on the spot. Just like that, they’ve slashed their costs and boosted their profit on every single sale that follows.

Meanwhile, the second business is always playing catch-up. Its cash is trapped in overdue invoices from customers and stock that’s gathering dust on the shelves. When that exact same discount offer comes their way, they have to let it pass. They simply don’t have the spare cash to make the move.

Turning Stress Into an Advantage

This isn’t just about missing out on a single deal. The business with its finances in order has the freedom to make smart plays that drive real growth.

- Hiring Top Talent: They can bring on a superstar salesperson right when they need one, grabbing more of the market while their competitor is just trying to make payroll.

- Investing in Better Gear: They can afford to upgrade their equipment, making them more efficient and improving their product quality—another leg up on the competition.

- Weathering Economic Storms: When an unexpected bill lands or sales take a dip for a month, they have a cash cushion to ride it out without breaking a sweat.

The business that’s ignoring its working capital? It misses every single one of these opportunities. Instead of focusing on growth, all its time and energy go into chasing payments and just trying to stay afloat.

At its core, solid working capital management turns what is normally a source of financial stress into a serious competitive advantage. It empowers you to be proactive instead of constantly being reactive.

This isn’t just a theory for small Kiwi businesses; it’s a strategy major global companies rely on to build resilience. After all the recent supply chain chaos, many large firms deliberately bulked up their working capital. That isn’t just cash sitting there doing nothing; it’s a war chest. You can read more on how companies manage liquidity to guard against disruptions and price volatility.

Ultimately, getting a handle on your working capital gives you control. It leads to better cash flow, healthier profits, and the financial strength to turn challenges into your next big opportunity.

Actionable Strategies to Improve Your Working Capital

Alright, you get the “what” and “why” of working capital. Now for the fun part: making real changes that put more cash in your pocket. Don’t worry, this isn’t about some massive, complex financial overhaul. It’s about smart, practical tweaks that give you breathing room.

The name of the game is shrinking your cash conversion cycle. Think of it as the journey your money takes – from the moment you pay for stock to the moment a customer’s payment lands in your bank account. The shorter that trip, the faster your cash comes home.

Here are a few real-world strategies you can put into practice today.

Tighten Up Your Invoicing

The second you finish a job or deliver that product, the clock starts ticking. Don’t let your invoices gather digital dust on your desktop. Get them out the door immediately. Modern cloud accounting software can handle this automatically, so nothing ever slips through the cracks.

A few simple but powerful tweaks can make all the difference:

- Offer every payment option under the sun. Make it ridiculously easy for customers to pay you. Bank transfer, credit card, online portals—the more options, the fewer excuses.

- Set crystal-clear payment terms. Don’t be vague. State firmly on every invoice whether payment is due in 7, 14, or 30 days. Be polite, but be firm.

- Automate your reminders. Let your accounting system play the role of a gentle nudge. A polite, automated reminder for an upcoming or overdue invoice saves you from making those awkward phone calls.

Master Your Inventory Control

If you’re an Auckland business selling physical goods, that stock on your shelves is literally cash just sitting there. Getting a handle on your inventory is one of the quickest ways to unlock it. The sweet spot is having just enough to meet demand without tying up precious funds in stuff that isn’t selling.

Start by getting forensic with your stock tracking. Know your bestsellers inside and out, and be honest about the slow-movers. Could you run a flash sale to clear out that older stock? A small discount now is far better than letting products collect dust and lose value indefinitely.

A tidy, organised stockroom is often a sign of a healthy, cash-flow-positive business. Every time you speed up your inventory turnover, you shorten that cash conversion cycle and get money back in your bank account faster.

As you explore how to balance what you own against what you owe, you can dig into some more proven strategies to improve working capital.

Forecast Your Cash Flow Religiously

Waiting for a surprise bill to discover you’re short on cash is a stressful way to run a business. This is where a simple cash flow forecast becomes your best friend. It’s nothing more than a schedule of all the money you expect to come in and all the money you expect to go out over the next few weeks and months.

This doesn’t need to be fancy. A basic spreadsheet is a great start. By mapping out your income and expenses, you can spot potential cash crunches long before they become a five-alarm fire, giving you plenty of time to react.

Choosing the Right Strategy for Your Business

Every Auckland business is unique, and there’s no single “best” way to manage working capital. A tradie in West Auckland has different challenges than a retailer in Newmarket. What matters is picking the strategy that fits your specific situation.

Here’s a quick comparison to help you see what might work for you.

Working Capital Strategies At-a-Glance

| Strategy | Best For… | Key Benefit | Potential Risk |

|---|---|---|---|

| Aggressive | Fast-growing, high-risk tolerance businesses (e.g., tech startups). | Maximises profitability by using short-term, low-cost debt. | High risk of cash shortages if sales dip or rates rise. |

| Conservative | Stable, risk-averse businesses (e.g., established professional services). | Low risk of insolvency; very stable cash position. | Lower profitability due to holding excess cash and long-term debt. |

| Moderate | Most SMEs, including retailers, hospitality, and construction. | A balanced approach, mixing short and long-term finance to manage risk. | Requires more active management to maintain the right balance. |

Ultimately, the goal is to find that perfect balance between having enough cash on hand to operate smoothly and putting your money to work to grow the business. Start with the moderate approach and adjust as you get a better feel for your cash flow rhythm.

Common Working Capital Traps to Watch Out For

They say we learn from our mistakes, but in business, learning from someone else’s is a whole lot cheaper. When it comes to your cash, certain mistakes are so common they’ve become predictable traps for busy small business owners. Knowing how to spot and sidestep these is crucial for staying in the game long-term.

It’s easy to fall into these traps. Most owners are laser-focused on making sales, forgetting that what happens to the money after the sale is just as critical. By understanding these common blunders, you can set up simple guardrails to keep your business safe.

Going All-In on Assets Too Early

It’s exciting to want the best gear right from the start. Who wouldn’t want a brand-new work truck, the flashiest coffee machine, or a top-of-the-line computer setup? But pouring a massive chunk of your cash into fixed assets before you really need them can choke the life out of your day-to-day operations.

Imagine an Auckland landscaping business taking out a huge loan for a big, expensive digger. It looks great on the yard, but it sits idle most of the week. Those hefty monthly repayments are a constant drain, leaving them scrambling to cover wages and fuel. The lesson? Start lean. Only upgrade to the big stuff when your cash flow proves you can comfortably afford it.

Being Too “Nice” About Getting Paid

Being a good sort is great for building relationships, but being too casual about customer payments is a one-way ticket to a cash flow disaster. Every time you let an invoice slide for 60 or 90 days, you’re effectively giving that customer a free loan—and you’re the one paying for it.

This is hands-down one of the most common and easily corrected mistakes we see. Your business isn’t a bank, and you simply can’t afford to fund your customers’ operations.

The fix is straightforward: set crystal-clear payment terms from day one. An Auckland-based tradie who switches their terms from a vague “due upon receipt” to a firm 14-day deadline can massively improve their cash position without coming across as pushy.

Letting Old Stock Gather Dust

That box of last season’s t-shirts or those out-of-date phone cases in the storeroom aren’t just taking up space—they’re holding your cash hostage. Hanging onto inventory that isn’t selling is a classic mistake that directly poisons your working capital. Every dollar tied up in that dead stock is a dollar you can’t use to pay suppliers or buy new products that people actually want.

The smart play here is to spot these slow-movers early and do something about it. Try a few of these tactics:

- Run a clearance sale: Getting 50% of your money back is infinitely better than getting 0%.

- Bundle it: Package a slow-moving item with a bestseller to create a more attractive deal.

- Use it as a bonus: Reward a loyal customer with a freebie and clear out the old stock at the same time.

Your Working Capital Questions, Answered

Once you get your head around the basics of working capital, a few practical questions almost always come up. It’s one thing to understand the theory, but it’s another thing entirely to know what it means for your business day-to-day. Let’s dig into some of the most common questions we hear from business owners right here in Auckland.

What’s a Good Working Capital Ratio?

You’ve probably heard of the working capital ratio (Current Assets / Current Liabilities). Think of it as a quick financial health check for your business, but what number should you actually be aiming for?

Generally speaking, a ratio between 1.2 and 2.0 is considered pretty healthy. This tells you that you have more than enough short-term assets on hand to cover your short-term debts, with a nice comfortable buffer.

But hold on—a number above 2.0 isn’t always the goal. It can actually be a sign that your business isn’t using its assets very well. You might have too much cash just sitting in a low-interest account, or maybe too much money is tied up in stock that simply isn’t selling.

The “ideal” ratio is less about a magic number and more about your specific situation. A ratio below 1.0 is a definite red flag, suggesting you might have trouble paying your immediate bills. But the perfect number really depends on your industry and business model.

A retailer stocking up for Christmas might temporarily have a higher ratio, and that’s fine. On the other hand, a service-based business with low overheads might run smoothly with a lower one. The trick is to know what’s normal for you and to notice any sudden, unexpected changes.

How Often Should I Check My Working Capital?

Please don’t treat this like a once-a-year task you only think about around tax time. For a small business, your working capital can change dramatically in just a few weeks. Leaving it unchecked for too long is like driving down the Southern Motorway with your eyes closed—it’s not going to end well.

For most small to medium businesses in Auckland, here’s a good rhythm to get into:

- Monthly Review: Set aside time once a month to properly calculate your working capital ratio and look at the key pieces. Check your aged receivables, your payables, and your stock levels. Are things trending in the right direction?

- Weekly Check-in: A quick, informal glance at your cash flow every week is crucial. This isn’t a deep dive. It’s just a simple check of your bank balance against upcoming payroll and major supplier bills to spot a potential shortfall before it becomes a full-blown crisis.

These regular check-ins transform what is working capital management from a chore you dread into a simple, powerful business habit.

Can I Have Too Much Working Capital?

It sounds like a dream problem, doesn’t it? But yes, you can absolutely have too much working capital. While it’s certainly safer than having too little, a pile of excess working capital often points to lazy money and missed opportunities.

Think of it this way: every dollar sitting idle in your bank account is a dollar that isn’t working for you. That extra cash could be doing much more productive things.

For instance, that surplus capital could be:

- Reinvested for Growth: Put towards new equipment, a fresh marketing campaign, or hiring that key person you need.

- Paying Down Debt: Used to knock down high-interest loans, which saves you a ton of money in the long run.

- Distributed to Owners: Returned to yourself or other shareholders as a well-earned profit.

An overly high working capital balance, especially if it’s just a big pile of cash, suggests your business is playing it too safe and possibly missing out on growth. The goal isn’t just to have capital, but to make that capital work hard for you.

Feeling like you’re just guessing when it comes to your business finances? At Business Like NZ Ltd, we help Auckland business owners move from confusion to clarity. We’re chartered accountants who specialise in giving you the practical advice you need to build a stronger, more profitable business. Let’s create your financial freedom together.