Master Your Cash Flow Forecast in NZ: Guide

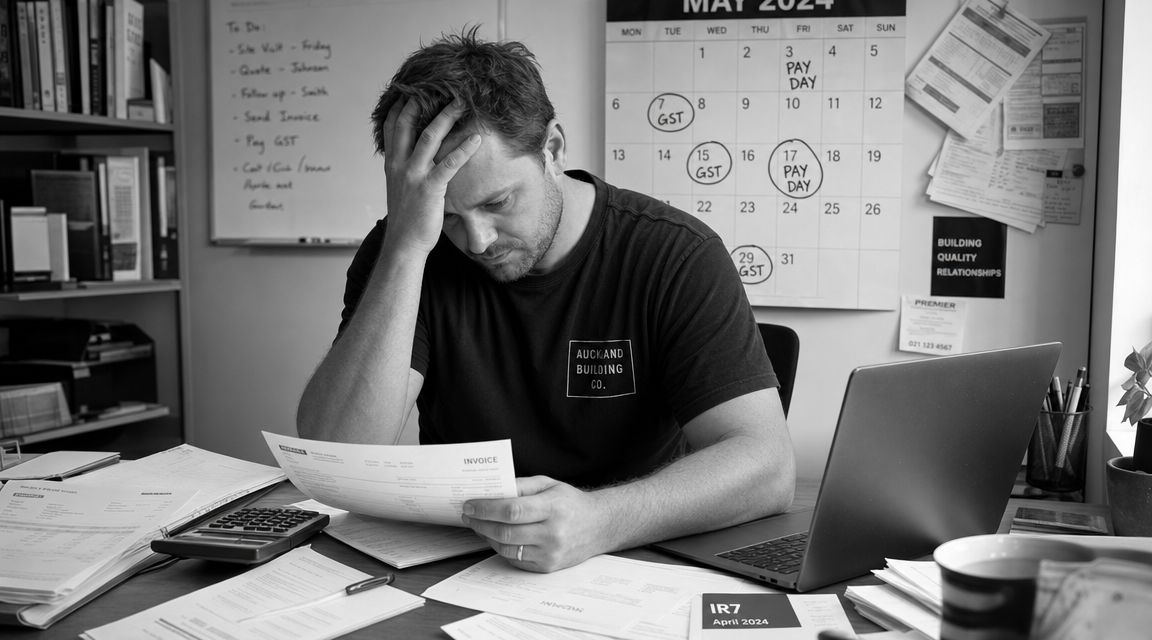

You're probably feeling this already. Sales are coming in, the phone keeps ringing, tenants are paying most of the time, and on paper things look fine. Then wages hit on Thursday, GST is due, a supplier wants paying now, and the bank balance tells a different story.

That's why a cash flow forecast matters. It doesn't tell you whether the business is “doing well” in a general sense. It tells you whether cash will be there when you need it.

Why Your Business Needs a Cash Flow Forecast

A cash flow forecast is a forward view of money coming into and leaving your bank account. It is not the same as a profit and loss report. Profit can look healthy while cash is tight, especially if customers pay late, tax falls due in a lump, or a property has an empty period. If that mismatch catches you out, this guide on why profit doesn't match your bank balance is worth reading.

For New Zealand businesses, this isn't a niche finance exercise. It's basic control. The 2023 Business Demography Statistics showed New Zealand had 551,000 active enterprises, and 97.2% were small enterprises with 0 to 19 employees, according to Lightspeed's summary of the Statistics NZ release. That tells you most local businesses operate without much room for timing mistakes.

Practical rule: If one delayed payment or one tax bill can put pressure on your account, you need a cash flow forecast.

For an Auckland tradie, that may mean checking whether next week's receipts cover wages and materials. For a property investor, it may mean knowing whether rent, rates, insurance, interest, and repairs line up cleanly over the next few months. Either way, the point is the same. You want to see the problem before the bank does.

Gathering Your Key Financial Inputs

Most forecasts go wrong before the first formula is entered. They start with incomplete information or unreconciled balances.

What to pull together first

Before you open Xero or a spreadsheet, gather these items:

- Reconciled bank balances. Start with what is in the bank, not what you think should be there.

- Customer invoices and expected payment dates. Not just invoice due dates. Use realistic collection timing.

- Supplier bills and regular payments. Include rent, wages, loan repayments, subscriptions, and insurance.

- Tax dates. Put GST, PAYE, and provisional tax into the calendar before anything else.

- One-off items. Repairs, equipment purchases, legal costs, bond refunds, or maintenance.

- Property-specific inflows and outflows. Rent, vacancies, rates, body corporate, maintenance, and mortgage payments.

What works better than guessing

A clean forecast starts from cash, then moves to timing. Don't build it off sales alone. Don't assume every invoice will be paid on the due date. And don't rely on the profit and loss report to answer a cash question. If you want a quick refresher on that report, see what a profit and loss statement is.

The best forecasts are usually boring. They're based on real bank balances, actual bills, and known payment dates.

Building Your Forecast in Xero or a Spreadsheet

For most Auckland SMEs, the most useful format is a 13-week weekly forecast. It should begin with reconciled cash, be rolled forward each week, separate contracted inflows from pipeline, and map outflows to actual payment dates, as outlined in Numeric's cash flow forecasting guide.

A simple structure that works

Use one row for each cash item and one column for each week.

Inflows

- Contracted cash from issued invoices, signed jobs, confirmed rent, or other committed receipts

- Pipeline cash kept separate so you don't treat possible work as banked money

- Other receipts such as loans, owner funds, or refunds if applicable

Outflows

- Wages and payroll costs

- Supplier payments

- Rent, rates, and utilities

- GST, PAYE, and provisional tax

- Debt repayments

- Repairs, maintenance, and one-off costs

Then calculate:

- Opening cash

- Plus inflows

- Less outflows

- Closing cash

That closing cash becomes next week's opening cash.

Using Xero without overcomplicating it

If you use Xero, keep the workflow practical. Reconcile the bank first. Review unpaid sales invoices, unpaid bills, payroll timing, and scheduled tax payments. Then build the forecast either in Xero's short-term cash tools or in a spreadsheet beside Xero if you want more control over timing and scenarios.

For business owners who want cleaner bookkeeping and better reporting habits, these Xero tips for small business are a good starting point.

A spreadsheet is still fine if it's kept current. In fact, many owner-managed businesses prefer it because they can see every payment date in one place. Property investors often like that format too, especially when they want to compare rent receipts against mortgage payments and expected maintenance.

Keep sales forecast and cash forecast separate. A signed contract is stronger than a verbal “should be fine”.

Business owners who want help setting up the first version can also work with an accountant. For example, Business Like NZ Ltd helps clients build and review working cash flow forecasts using Xero and simple reporting tools.

Using Scenario Planning to Reduce Risk

A single forecast isn't enough. It gives one version of the future, usually the version where everything goes roughly to plan.

A better approach is to test what happens when timing shifts. Intuit's treasury guidance notes that a stronger forecast does not rely on one average “days to pay” assumption. It stress-tests what happens if one or two major customers pay late, which matters when funding conditions are under pressure.

Useful scenarios for Auckland SMEs

Try these three:

- Late payment scenario. A key customer pays later than expected.

- Tax pressure scenario. GST or provisional tax falls due in the same period as a weak sales month.

- Property shock scenario. A tenancy turns over, rent pauses, and a repair bill lands close together.

What you're looking for

You're not trying to predict every problem. You're checking how quickly cash tightens and what action you'd take.

That action might be slowing discretionary spending, following up debtors earlier, moving supplier timing, holding back drawings, or setting aside tax money sooner. A forecast becomes much more useful once it starts shaping decisions, not just recording expectations.

Common Forecasting Mistakes to Avoid

The most common mistake is treating invoices as cash. They're not. Cash lands when the customer pays, not when you raise the invoice.

Another big one is missing tax timing. A forecast that only shows sales and supplier payments can miss GST, PAYE, and provisional tax instalments, which can create a cash shock.

A short checklist

- Don't start unreconciled. If the opening bank balance is wrong, the whole forecast is wrong.

- Don't smooth collections. Use likely payment timing, not ideal timing.

- Don't forget lump-sum outflows. Tax, insurance, repairs, and debt payments matter.

- Don't leave it static. Update actuals and roll it forward.

Good forecasting can be very accurate, but only when it's refreshed often and based on clean cash data, as noted earlier in the article.

Frequently Asked Questions

How often should I update my cash flow forecast

Bi-Weekly is the best rhythm for most small businesses. Replace the prior week's forecast with actuals, review the gaps, and roll the model forward. Good cash forecasting can achieve up to 90% quarterly accuracy when assumptions are controlled and forecasts are refreshed frequently, according to EY's cash forecasting guidance.

What's the difference between cash flow and profit

Profit includes income earned and expenses incurred, whether or not cash has moved. Cash flow looks at when money arrives and leaves. That's why a profitable business can still feel squeezed.

Can I do my own forecast or should I get help

You can do your own if your records are up to date and you're willing to review it regularly. Many owners start with a spreadsheet and Xero data. If tax dates, multiple properties, debt repayments, or uneven customer payments make things messy, getting an accountant to set up the structure can save a lot of rework.

If you want help putting a practical cash flow forecast in place, Business Like NZ Ltd supports Auckland businesses and property investors with affordable, down-to-earth chartered accounting advice. They can help you set up a forecast that's simple to maintain, tied to real payment dates, and useful for day-to-day decisions.