Accounting Advice Tips for Small Business Success

Level Up Your Business Finances

Running a small business in Auckland? Want better financial management? This listicle provides eight essential accounting advice tips for small businesses to boost your bottom line. Learn how to separate business and personal finances, leverage cloud accounting software, track expenses, manage taxes, and more. These practical tips will help you stay organized, compliant, and profitable. Following these accounting best practices ensures accurate financial reporting and informed decision-making, setting your business up for success.

1. Separate Business and Personal Finances

One of the most fundamental pieces of accounting advice for any small business, especially in Auckland’s competitive market, is to separate business and personal finances. This crucial step involves establishing distinct boundaries between your company’s financial activities and your own. Practically, this means opening dedicated business bank accounts (both checking and savings), obtaining separate business credit cards and lines of credit, and meticulously maintaining separate records for all business transactions. This separation isn’t just a good idea; it’s often a legal requirement for incorporated entities like companies and lays the groundwork for sound financial management.

This practice is paramount for several reasons. Firstly, it drastically simplifies tax preparation and significantly reduces your audit risk. The Inland Revenue Department (IRD) requires accurate and verifiable records, and commingling funds makes it difficult to differentiate between business expenses and personal spending. Secondly, separating finances provides a crystal-clear picture of your business’s profitability. By tracking income and expenses in dedicated accounts, you gain valuable insights into your cash flow, identify areas for improvement, and make informed decisions about pricing, investment, and growth. For Auckland businesses facing a dynamic economic landscape, this financial clarity is essential for sustainable success.

Furthermore, separating business and personal finances safeguards your personal assets from potential business liabilities. In the unfortunate event of a lawsuit or bankruptcy, your personal savings, house, and other assets are protected if your business finances are kept separate. This separation acts as a shield, limiting your personal exposure to business risks. This protection is particularly crucial in Auckland, where the cost of living is high and safeguarding personal assets is a priority.

Implementing this separation provides tangible features and benefits. Dedicated business checking and savings accounts offer a professional image and enable you to manage your business finances efficiently. Separate business credit cards and lines of credit help build a business credit history distinct from your personal credit, opening up more financing options in the future. Distinct record-keeping systems for business expenses, coupled with a clear documentation trail for all business transactions, provide the necessary evidence for tax purposes and financial reporting. Building professional business banking relationships can also lead to valuable advice and support as your business grows.

- To make this process smoother, consider the following tips:

- Automated Transfers: Set up automatic transfers from your personal to business accounts for initial funding and regular contributions.

- Business Debit Cards: Use business debit cards instead of cash whenever possible for better tracking and record-keeping.

- Regular Reconciliation: Review and reconcile your business accounts weekly or monthly to catch errors early and maintain accurate financial records.

- Integrated Software: Consider banks that offer integrated accounting software connections to streamline your financial management.

- Document Personal Fund Use: Document any legitimate business use of personal funds immediately, including reimbursements, to maintain clarity and avoid confusion during tax season.

By diligently separating your business and personal finances, you establish a solid foundation for accurate accounting, informed decision-making, and long-term financial health for your Auckland business. This proactive approach not only fulfills legal requirements but also positions your business for sustainable growth and success in a competitive market.

2. Implement Cloud-Based Accounting Software

As a small business owner in Auckland, efficiently managing your finances is crucial for success. One of the most impactful pieces of accounting advice for small business is to implement cloud-based accounting software. This modern approach offers professional-grade financial management tools, previously only accessible to large corporations, now readily available and affordable for businesses of all sizes. These platforms automate tedious accounting tasks, provide real-time financial insights, and enhance data security through cloud storage, streamlining your financial operations and freeing up valuable time to focus on growing your business.

Cloud-based accounting software operates by securely storing your financial data on remote servers, allowing you to access it anytime, anywhere, with an internet connection. These platforms typically integrate with your bank accounts, payment processors, and other business tools, creating a comprehensive financial management ecosystem. This integration automates tasks like importing transactions and categorizing them, drastically reducing manual data entry and the risk of human error.

Key Features and Benefits:

- Automated Bank Feeds: Automatically imports and categorizes transactions from your bank accounts.

- Invoicing and Payments: Create professional invoices, track payments, and send automated reminders.

- Expense Tracking: Capture receipts with your phone, categorize expenses, and generate expense reports.

- Real-time Reporting: Access dashboards and reports that provide up-to-the-minute insights into your finances.

- Multi-User Access: Grant access to team members or your accountant with customized permission levels.

- Integrations: Connect with your bank, payment processors, e-commerce platforms, and other business tools.

Pros:

- Reduces manual data entry and human error.

- Provides real-time access to financial data from anywhere with an internet connection.

- Automatic software updates and security patches.

- Scalable to accommodate business growth.

- Often more cost-effective than hiring a full-time bookkeeper.

Cons:

- Monthly subscription costs can add up.

- Requires a reliable internet connection.

- Can have a learning curve for new users.

- Data security relies on the provider’s systems.

- May have limitations for very complex accounting needs.

Tips for Implementing Cloud-Based Accounting Software:

- Start Simple: Begin with the basic features and gradually add complexity as you become more comfortable with the system.

- Free Trials: Take advantage of free trials offered by different platforms to find the best fit for your business.

- Integration Check: Ensure your chosen software integrates with your existing bank accounts and payment systems.

- Automation Rules: Set up automated rules for common transaction categorizations to save time and improve accuracy.

- Regular Backups: Even though data is stored in the cloud, regularly back up your financial information as an added precaution.

3. Maintain Detailed Expense Tracking and Receipt Management

Effective accounting is the backbone of any successful small business, and for Auckland businesses, meticulous expense tracking is no exception. This isn’t just about keeping records; it’s about gaining a deep understanding of where your money is going, maximizing tax deductions, and ultimately, boosting your bottom line. Maintaining detailed expense tracking and receipt management is a cornerstone of sound financial practice, providing valuable insights into spending patterns, simplifying tax compliance, and paving the way for informed financial decisions. This detailed approach to expense management is particularly crucial for small businesses in Auckland’s competitive landscape, offering a significant advantage in managing resources and ensuring long-term sustainability.

For example, a construction contractor in Auckland might use a digital receipt capture app like Hubdoc to photograph and categorize material receipts directly on job sites, eliminating the risk of lost paperwork and ensuring accurate expense allocation to each project.

Implementing robust expense tracking offers a range of benefits for Auckland businesses:

Pros:

- Maximizes tax deductions and reduces tax liability: Accurate expense records allow you to claim all eligible deductions, minimizing your tax burden and maximizing your profits.

- Provides detailed insights into spending patterns: Understand where your money is going and identify areas for potential savings.

- Simplifies tax preparation and audit defense: Organized records make tax time less stressful and provide a solid defense in case of an audit.

- Helps identify unnecessary expenses and cost-cutting opportunities: Analyze spending patterns to pinpoint areas where you can trim expenses without impacting your business operations.

- Improves cash flow management and budgeting accuracy: Gain a clearer understanding of your cash flow and create more accurate budgets.

Cons:

- Requires consistent daily or weekly attention: Maintaining accurate records requires ongoing effort.

- Can be time-consuming for businesses with many transactions: Businesses with high transaction volumes might find the process time-consuming.

- Risk of losing receipts or documentation: Physical receipts can be easily lost or damaged.

- May require additional software or apps: Digital solutions often come with a subscription fee.

- Complex categorization rules can be confusing: Understanding tax codes and expense categories can be challenging.

Actionable Tips for Auckland Businesses:

- Photograph receipts immediately after purchases using smartphone apps: This ensures you never lose a receipt and simplifies record-keeping.

- Set up weekly recurring calendar reminders for expense review: Regular review helps you stay on top of your expenses and catch errors early.

- Create custom categories that match your specific business needs: Tailor your expense categories to reflect your unique business operations.

- Keep a mileage log in your vehicle for business travel: Track all business-related mileage for accurate deduction claims.

- Review and reconcile expense reports monthly to catch errors: Regular reconciliation ensures your records are accurate and up-to-date.

- Train employees on proper expense submission procedures: Consistent procedures ensure everyone is on the same page and simplifies record-keeping.

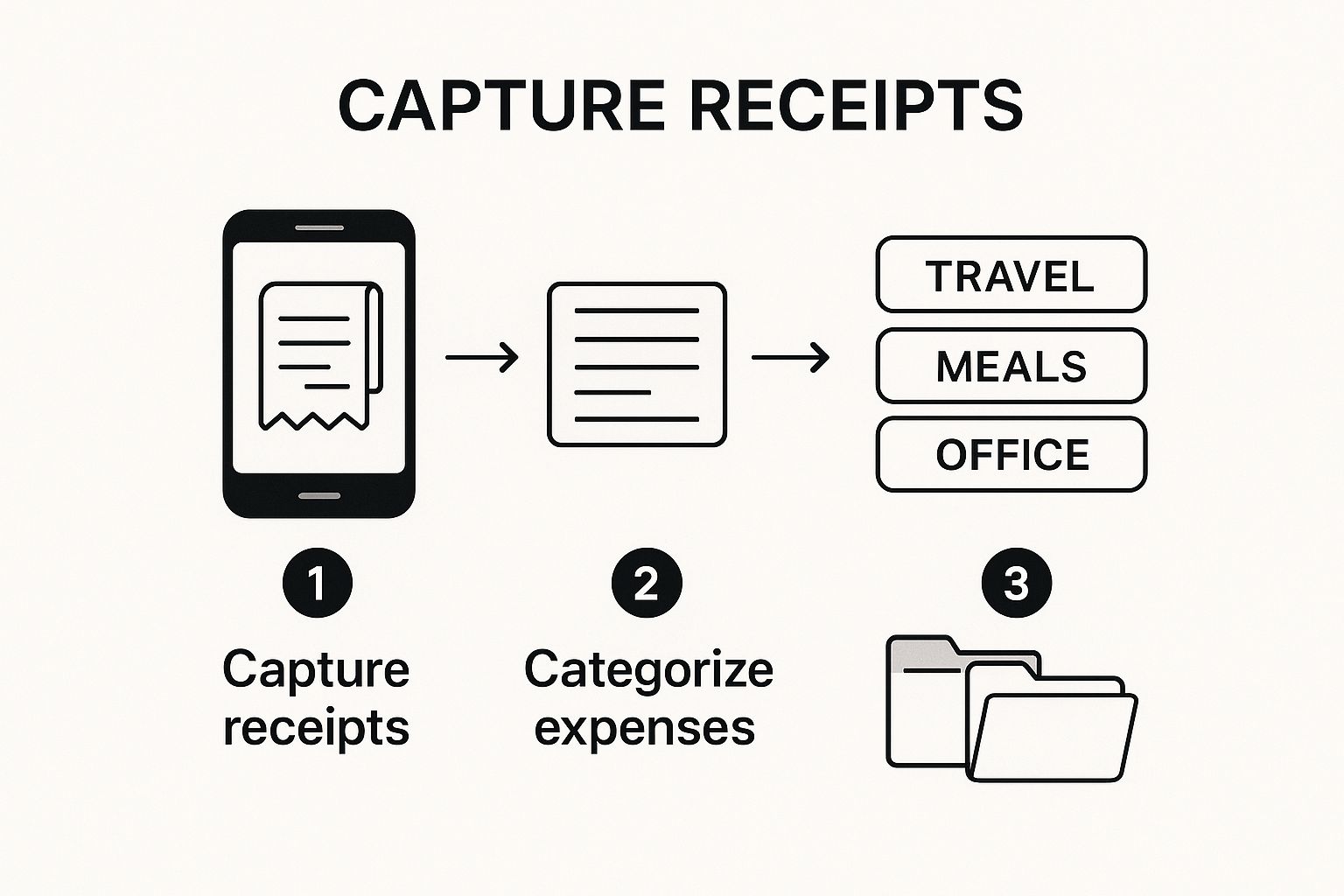

The following infographic illustrates a simple three-step process for efficient expense tracking:

This infographic visualizes a streamlined expense tracking workflow, starting with capturing receipts digitally, then categorizing them appropriately, and finally, storing them securely. This simplified process highlights how small businesses can leverage technology to manage expenses effectively, ensuring accuracy and accessibility for tax purposes and financial analysis. By following these steps, businesses can establish a robust system for managing expenses, ensuring compliance and informed decision-making.

By following these tips and embracing detailed expense tracking, your Auckland business can gain a competitive edge, optimize financial performance, and pave the way for long-term success. Don’t just track expenses – analyze them, learn from them, and use them to drive better business decisions. This is crucial accounting advice for any small business looking to thrive in the Auckland market.

4. Establish Regular Monthly Financial Reviews and Reconciliation

As a small business owner in Auckland, you’re likely juggling multiple responsibilities, and accounting might not be at the top of your list. However, dedicating time each month for financial reviews and reconciliation is crucial for the long-term health and success of your business. This process, a cornerstone of sound accounting advice for small business, involves meticulously comparing your internal business records with external statements from banks, credit card companies, and other financial institutions. This ensures accuracy, completeness, and gives you a clear picture of your financial standing. It’s not just about balancing the books; it’s about gaining control over your finances and making informed decisions that drive growth.

Monthly financial reconciliation involves reviewing every transaction, identifying any discrepancies between your records and bank statements, and updating your accounting records accordingly. This process culminates in generating key financial reports, such as your Profit & Loss statement, Balance Sheet, and Cash Flow statement, which provide valuable insights into your business performance. These reports are essential for understanding profitability, liquidity, and the overall financial health of your Auckland business.

Think of it like this: regular reconciliation is like getting a regular health check-up for your business finances. Early detection of errors, whether a simple $50 typo or a more significant issue, can prevent costly mistakes down the line, especially when it comes to tax time.

5. Understand and Plan for Tax Obligations

One of the most crucial aspects of accounting advice for small business, especially in Auckland, is understanding and planning for your tax obligations. Ignoring this aspect can lead to significant financial penalties, stress, and even legal issues. Proactive tax planning, on the other hand, allows you to minimize your tax liability legally, improve cash flow predictability, and focus on growing your business. This is especially relevant for small businesses in Auckland, facing a dynamic economic environment and specific regional tax regulations.

Tax planning for small businesses involves understanding the various types of taxes you might be liable for and implementing strategies to manage them effectively. These obligations can include income tax, self-employment tax (if you’re a sole proprietor or freelancer), payroll tax (if you have employees), and Goods and Services Tax (GST) in New Zealand. Each of these taxes has its own set of rules, deadlines, and reporting requirements. Failing to comply with any of these can result in penalties and interest charges, eating into your profits.

How Tax Planning Works:

Effective tax planning is an ongoing process, not a one-time event. It begins with understanding your specific tax obligations based on your business structure (sole proprietorship, partnership, or company), industry, and revenue. Here’s a breakdown:

- Quarterly Estimated Tax Payments: In New Zealand, provisional tax is payable in three installments throughout the year. Calculating and paying these estimated taxes on time avoids penalties and interest.

- Comprehensive Deduction Tracking: Keeping meticulous records of all eligible business expenses is crucial. These deductions can significantly reduce your taxable income. Common deductible expenses include rent, utilities, office supplies, marketing costs, and vehicle expenses (if used for business purposes).

- Payroll Tax Management: If you have employees, you’re responsible for deducting Pay As You Earn (PAYE) tax, KiwiSaver contributions (if applicable), and ACC levies from their wages and remitting them to the Inland Revenue Department (IRD).

- GST Collection and Remittance: If your turnover exceeds the GST registration threshold (currently NZD $60,000), you must register for GST. This involves collecting GST on your sales and paying GST on your purchases. You then file GST returns, typically every two months, and pay the net GST amount to the IRD.

- Tax Calendar Management: Maintaining a tax calendar with all relevant deadlines (provisional tax dates, GST filing dates, annual income tax return deadline) is essential for staying organized and avoiding late filing penalties.

Examples of Successful Implementation:

- A consulting firm in Auckland sets aside 30% of each invoice payment into a dedicated tax savings account. This ensures they have the funds readily available for their provisional tax payments.

- A photography studio in Auckland maximizes depreciation deductions on their expensive equipment through the depreciation rules outlined by the IRD, minimizing their taxable income.

Actionable Tips for Auckland Small Businesses:

- Open a separate bank account specifically for tax payments: This helps you segregate tax funds and avoid accidentally spending them.

- Calculate and save estimated taxes with each payment received: This makes paying provisional tax less daunting.

- Keep detailed records of all business expenses throughout the year: Use accounting software or a spreadsheet to track every expense. Keep receipts and invoices as proof.

- Consider business structure changes that might reduce your tax burden: Consult with a tax advisor to determine the most tax-efficient structure for your business.

- File tax extensions if needed, but always pay your estimated taxes on time: An extension gives you more time to file your return, but it doesn’t postpone your tax payment deadline.

Pros and Cons of Proactive Tax Planning:

Pros:

- Avoids costly penalties and interest charges.

- Maximizes available deductions and credits.

- Improves cash flow through predictable tax payments.

- Reduces stress during tax season.

- Ensures compliance with complex tax regulations.

Cons:

- Requires ongoing attention throughout the year.

- Tax laws can change, requiring you to stay updated.

- May require professional assistance, which can incur costs.

- Quarterly payments can strain cash flow for seasonal businesses.

By understanding and proactively planning for your tax obligations, you can establish a strong financial foundation for your Auckland small business, allowing you to focus on growth and success. Resources like the IRD website, tax professionals, and accounting software can provide valuable support in navigating the complexities of the New Zealand tax system.

6. Implement Proper Invoice Management and Accounts Receivable Tracking

Effective invoice management and accounts receivable (AR) tracking are crucial for the financial health of any small business, especially in a competitive market like Auckland. This process encompasses everything from creating and sending invoices to collecting payments and managing overdue accounts. For small businesses in Auckland looking for sound accounting advice, prioritizing this area can significantly improve cash flow, reduce administrative headaches, and foster stronger customer relationships. This makes it a vital element of any successful business strategy.

Think of your invoices as the lifeblood of your business. They’re how you get paid for the products or services you provide. A robust invoice management system ensures you’re paid on time, minimizing the risk of late payments and potential cash flow issues. This is particularly important for small businesses in Auckland, where managing expenses and maintaining a positive cash flow can be challenging. Ignoring this aspect of your business can lead to significant financial strain and hinder your ability to grow and thrive.

How Does It Work?

Effective invoice management starts with professional-looking invoices that clearly outline the goods or services provided, the amount due, and the payment terms. This sets the stage for clear communication with your clients. Next comes timely delivery of these invoices, whether through email, postal mail, or an integrated online system. Once invoices are sent, the system should allow you to track their status – paid, unpaid, or overdue. Automated reminders are a key component, gently nudging clients about outstanding payments. Finally, the system should generate reports that provide insights into your accounts receivable, such as aging reports that identify chronically late-paying customers.

Features of a Good System:

- Professional Invoice Templates: Use templates that include your business logo, contact information, and clear payment terms.

- Automated Invoice Generation and Delivery: Streamline the invoicing process and reduce manual effort.

- Payment Tracking and Aging Reports: Monitor outstanding invoices and identify potential problem areas.

- Automated Reminder Systems: Politely remind customers about overdue payments without straining relationships.

- Multiple Payment Method Acceptance: Offer convenience to your Auckland customers by accepting credit cards, ACH, and online payments.

- Customer Credit Management and Payment History Tracking: Build a clearer picture of your customer’s payment behavior to mitigate risks.

Examples of Successful Implementation in Auckland:

- A web design agency in Parnell uses automated invoicing to bill clients upon project milestone completion, ensuring prompt payment for their work.

- A consulting firm in the CBD implements net-15 payment terms with a 2% early payment discount, incentivizing faster payment and improving cash flow.

Pros:

- Improves Cash Flow: Faster payment collection translates directly to improved cash flow.

- Reduces Administrative Time: Automation frees up valuable time for other business activities.

- Professional Image: Professional invoices reflect positively on your business.

- Better Financial Forecasting and Planning: Accurate AR data facilitates more accurate forecasting.

- Reduces Bad Debt Losses: Proactive tracking and follow-up minimize the risk of uncollected payments.

Cons:

- Requires Consistent Follow-Up: Managing overdue accounts requires diligence and persistence.

- Potential Strain on Customer Relationships: Handling late payments requires tact and professionalism.

- Processing Fees for Electronic Payments: While offering convenience, electronic payments incur fees.

- Time Investment in Setup and Maintenance: Implementing and maintaining a system requires initial time and effort.

Actionable Tips for Auckland Businesses:

- Send invoices immediately upon completion of work or delivery.

- Offer multiple payment options, including popular methods in New Zealand.

- Include clear payment terms and late fee policies on all invoices.

- Follow up on overdue accounts promptly but professionally, keeping in mind the local business culture.

- Consider offering early payment discounts to improve cash flow.

- Implement credit checks for large new customers, particularly in industries with higher risk.

By implementing proper invoice management and accounts receivable tracking, small businesses in Auckland can significantly enhance their financial stability and operational efficiency. This system is not just about getting paid; it’s about building strong financial foundations, fostering positive customer relationships, and ultimately, contributing to the long-term success of your business in the vibrant Auckland market.

7. Monitor Cash Flow and Create Financial Forecasts

For Auckland small businesses seeking sound accounting advice, mastering cash flow management and financial forecasting is paramount. This isn’t just another accounting task; it’s the lifeblood of your business, directly impacting your ability to thrive and navigate the often turbulent waters of the Auckland market. Effective cash flow management, combined with accurate financial forecasting, provides the financial roadmap you need to make informed decisions, plan for growth, and ultimately achieve long-term success. This crucial practice often marks the difference between a flourishing business and one struggling to stay afloat, especially for small businesses with limited financial reserves.

Imagine a seasonal retailer in Auckland. They can leverage cash flow forecasts to strategically plan inventory purchases for peak seasons like Christmas or summer holidays, ensuring they have enough stock to meet demand without overspending. Similarly, they can optimize staffing levels, anticipating periods of high customer traffic and ensuring adequate coverage while managing labor costs effectively. This foresight prevents overstocking and overstaffing during slower periods, preserving valuable cash resources.

The advantages of implementing robust cash flow monitoring and forecasting are numerous. It provides an early warning system for potential cash shortfalls, allowing you to take corrective action before a crisis hits. It empowers you to make strategic decisions based on data-driven financial projections rather than relying on guesswork. Furthermore, the transparency it offers improves relationships with lenders and investors, demonstrating your financial acumen and responsible management. Forecasting also helps optimize the timing of major purchases and investments, ensuring you make these decisions when your financial position is strongest. Finally, by analyzing historical data, you can identify seasonal patterns and business cycles specific to the Auckland market, enabling you to anticipate fluctuations in demand and adjust your operations accordingly.

However, like any valuable tool, it requires diligent effort. Regular time investment and attention to detail are crucial for accurate tracking and forecasting. Forecasts, especially for new businesses in Auckland, may be inaccurate due to limited historical data. Furthermore, projecting potential problems can understandably create anxiety, although being forewarned allows for proactive solutions. Finally, effective forecasting requires a thorough understanding of your business drivers and market conditions, which may necessitate ongoing learning and adaptation.

Learn more about Monitor Cash Flow and Create Financial Forecasts

Here are some practical tips for Auckland small businesses looking to implement effective cash flow management and forecasting:

- Update forecasts weekly: Incorporate actual results and revise projections to maintain accuracy.

- Be comprehensive: Include all known future expenses, including taxes, loan payments, and rent.

- Build in a buffer: Establish cash reserves for unexpected expenses or unforeseen opportunities.

- Be conservative with revenue and liberal with expenses: This cautious approach provides a more realistic financial picture.

- Track key performance indicators (KPIs): Identify the metrics that directly influence your cash flow, such as sales conversions or customer acquisition costs.

- Proactive lender relationships: Cultivate relationships with lenders before you need financing, establishing trust and facilitating access to capital when needed.

By diligently monitoring your cash flow and creating accurate financial forecasts, you gain a powerful advantage in the competitive Auckland business landscape. This proactive approach to financial management allows you to anticipate challenges, capitalize on opportunities, and confidently navigate your business towards sustainable growth and success. This deserves its place in this list of accounting advice for small businesses as it is a cornerstone of financial health and stability.

8. Work with Qualified Accounting Professionals

Sound accounting practices are the bedrock of any successful small business. While you might handle basic bookkeeping yourself, especially in the early stages, partnering with qualified accounting professionals is invaluable for long-term financial health and growth. This crucial piece of accounting advice for small business can significantly impact

What can accounting professionals do for your business?

A qualified professional can handle a wide range of accounting tasks, including:

- Professional bookkeeping and financial statement preparation: Accurate and up-to-date financial statements are crucial for understanding your business’s performance and making informed decisions.

- Tax planning and preparation services: Minimizing your tax burden while remaining compliant requires specialized knowledge. Tax professionals can help you take advantage of deductions and credits you might otherwise miss.

- Business advisory and strategic planning consultation: Beyond crunching numbers, experienced accountants can offer valuable insights into your business strategy, helping you identify opportunities for growth and cost savings.

- Payroll processing and compliance management: Managing payroll can be complex, especially as your team grows. Professionals ensure accurate and timely payments while adhering to all relevant regulations.

Pros:

- Ensures compliance with tax laws and regulations: Avoid costly penalties and legal issues by staying compliant.

- Provides expertise for complex transactions and decisions: Navigate complex financial situations with confidence.

- Saves time, allowing you to focus on core business activities: Delegate time-consuming accounting tasks so you can concentrate on growing your business.

- Often pays for itself through tax savings and efficiency improvements: The money saved through optimized tax strategies and streamlined processes can outweigh the cost of professional services.

- Provides credibility with lenders, investors, and partners: Demonstrate financial stability and professionalism.

Ready to Streamline Your Business Accounting?

Running a small business in Auckland is demanding, but mastering your finances doesn’t have to be. This article has provided essential accounting advice for small business owners, covering everything from separating personal and business finances to leveraging cloud-based software, managing invoices, and planning for tax obligations. By implementing these strategies—detailed expense tracking, regular financial reviews, and cash flow monitoring—you’ll gain invaluable insights into your business’s performance and be better prepared for future growth. These practices are fundamental to not just surviving, but thriving in today’s competitive market.

Taking control of your accounting allows you to make informed decisions, optimize profitability, and ultimately focus on what matters most: growing your business. Remember that consistent effort, combined with the right tools and support, will lay a solid foundation for long-term financial success.

Looking for personalized accounting advice for small business needs in Auckland? Business Like NZ Ltd offers expert accounting, taxation, and business advisory services tailored to help you navigate the complexities of financial management and achieve your business goals. Visit Business Like NZ Ltd today to learn more and unlock your business’s full potential.